Happy Holidays to all my peers in the Accounts Receivable Management (ARM) industry! With the tax season upon us, it is holiday season for businesses of every kind who will be marketing at the discretionary dollars consumers will be receiving from their 2015 tax refunds. Whether it is a furniture store or car dealership, companies are already bombarding consumers with incentives to cash in their tax refund while the getting is good. ARM companies are no different as we make tax season settlement offers, however with the billions of dollars of dormant judgement inventory in the market today shifting to garnishments may prove to be a more successful tax season strategy.

When you consider the lifecycle of a file, it is typically in the pre-judgment status for a very short period of time. On average, it takes 12 months from the placement date of a new file to reach a judgment status and that is being conservative. When you then take into account states like Arizona or Pennsylvania that have the shortest statue on judgments (at 4 years) compared to states like Illinois or Alabama that have the longest statue on judgments (20 years), a file is in the pre-judgment status for 5-25% of its lifecycle. Given how quickly a file progresses to judgment status, every law firm will have a surplus of dormant judgements to target this tax season.

Think about it…your judgment inventory is where you can turn legal strategy non-believers into believers. Judgments accounts are also where you will find the best opportunities to increase firm profitability. As we have previously discussed, if we take your firm’s entire list of expenses and divide it against the number of files you have received, we will come up with a cost per file. Next, take the cost per file and multiply it against all of your non-paying open judgments and this is what I call potential profit! Given it is the holiday season for ARM companies, I want to share the gift of an additional perspective.

The Four Keys to having a great dormant judgment strategy are:

1. Have a defined process when entering judgments.

You would not believe how many files I have seen get swept over because a staff member “forgot” or “missed” an employer or bank on file. Take the time to create an If-Then statement to prevent these errors.

If-Then statement example: If the file has a bank or an employer and there is no reason to send it out of garnishment (return mail, payment arrangement, close code, dispute etc.) then place it into garnishment status.

2. Pay your collectors a bonus based off of the first garnishment payment.

Collectors are just like anyone else. Their actions and behavior are based off of incentives. We all have compliance incentives and company policy incentives, but you must also have an incentive program for garnishment!

As an example, I have seen collectors hold files from garnishment to get a consumer to send in a payment that was months past due. When I inquired further into their motivation around holding a file back from garnishment, the answer was simple – there is no incentive for garnishments. The following month we implemented an incentive program for first payments and our garnishments went up 25%.

3. Have a process for scanning incoming checks.

Everyone has consumers that send in checks without speaking to anyone in the office. Consumers can forget to inform you of new addresses, telephone numbers, and bank information. It is very easy to setup a process to scan in the check at the time of payment, verify the data in the check, and compare it against the data you already have.

Here is an example of a process I have seen work well. If a consumer does not have a bank on file, once the check is scanned in, the system sees the blank field and automatically adds the bank to the file. I love free data!

4. Buy employer and bank data from more than one vendor.

Sounds simple right? You would be surprised by how many firms I have spoken with that do not purchase data. Wayne Gretsky once said, “You miss 100% of the shots you don’t take.” If you are not buying assets today you are leaving money on the table. In my opinion, it is a complete waste of money to bring a file to a judgment status only to let it sit there and collect dust.

Another strategic mistake I see firms making is they rely on only one asset vendor. I have spent years developing and testing different data sources and one thing that is for certain is there is no magic bullet when it comes to deploying an asset strategy. If you want to be successful at unlocking the value of your judgment accounts, you must take multiple shots using different vendors to locate assets. From my experience, it is optimal to have 4 vendors for employment data and another 4 vendors for bank data (if your state allows). Having this many vendors might sound like a lot to manage, but it is worth your time if your firm executes the strategy correctly.

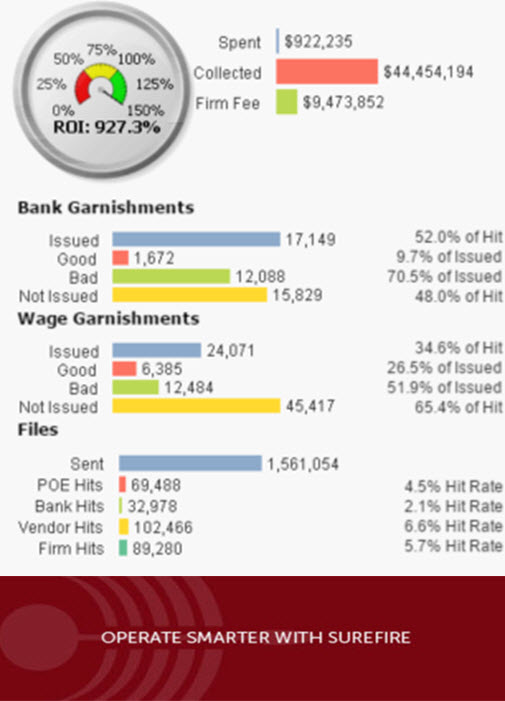

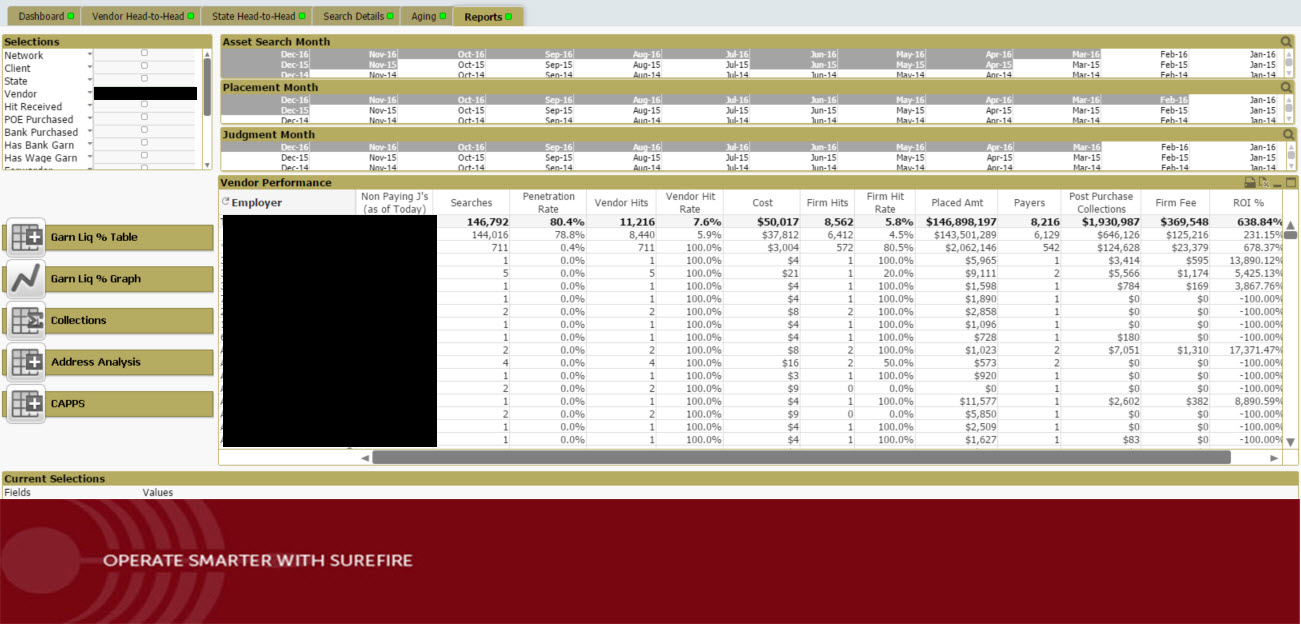

For this strategy to work, ARM companies must have a system in place to track the performance of each vendor. Being able to access KPIs such as Searches by Vendor, Hit Rate by Vendor, Hit Cost by Vendor, Placed Amount by Vendor and ROI by Vendor is paramount.

In addition, ARM companies purchasing assets should develop their own internal database of employers and banks they previously tried from other vendors. Having access to your historical results will help you identify scenarios where Vendor #3 in your waterfall provides you with an asset that you already received from Vendor #1 or Vendor #2. Tracking the results this way will help your firm understand the quality of the hits (SSI, Retired, Self-Employed, etc.) you are receiving by vendor and it will also allow you to expedite any refunds owed by your vendor.

Below is an application we developed, Surefire Waypoint, to help our clients operate smarter with their judgment inventory. If your firm is interested in collecting more money during tax season, we would be more than happy to schedule a meeting!