‘Tis the season…Settlement Letter season! Barely a day has passed, since the first week of January, that we haven’t received a client request to send settlement letters on their accounts. Some clients have even gone so far to provide us their own “special letter” using their language (Awesome!).

Without proper preparation and a sound strategy, I honestly feel we could call the first quarter “how to waste money on postage season”!

Over my 20+ years in this industry, here are 4 mistakes I review and reference during this time of the year.

Mistake Number 1: Talking to the consumer as if you are writing a legal brief.

In the ARM industry today (and probably for the rest of our lives) “compliance” should be the number one focus of any firm. If compliance is not your number one concern well…”Houston we have a problem”. While focusing on staying compliant with FDCPA, UDAAP, and State Laws, I feel it is vitally important to still speak to the consumer as a human being!

The reason why we have our compliance staff is to make sure every “t is crossed” and every “I is doted”…the letter doesn’t have to be as sterile as a surgical room to be compliant. The quickest way to improve your results is to write your settlement letter the same way you would talk to your neighbor. I understand that we have to have disclosers in each letter but your opening paragraphs do not need to read like a prescription drug pamphlets. The easiest way to find out if you fall into this category is take your letter template home tonight and read it to someone not in the business and see their reaction. Watch their face!

Mistake Number 2: Making the consumer call your collectors to take advantage of the settlement offer.

We live in a world where we do not want to speak to anyone! Think about the last time you called anyone outside of a client, friend or a loved one. If you are anything like me…your mind was listing all the other things you could be doing instead of being on the phone! I personally do not enjoy calling my cable company, cell phone company or call dealership. Going through the IVR, hitting each prompt just to maybe speak to someone about the problem I am having.

In my opinion the ARM industry is doing it all wrong making the consumer call you. We live in a world in which we are trying to get 8,000 things done each day and I am looking to accomplish each task with ease and quickness. If I have a consumer that wants to take advantage of an offer that I mailed them, I want them to go to my website. Not only is this convenient for the consumer since they can do it anytime they want but it is so much faster. With compliance as the number one rule our average talk time with the consumer has gone through the roof. My goal is to take make it as easy as possible for the consumer and that starts with the website. Another way to describe this is that you are buying shoes at a shoe store. You walk up to the counter you put the shoes down and hand the clerk your debit card. The clerk turns to you and says I understand you want to buy these shoes but I need to talk to you for the next 20 minutes before I ring up the sale. Personally I would walk out of the store pull out my phone and I buy them online. If you don’t have a website that accepts payments, first you should get one sooner than later and second allow them to use snail mail to take advantage of your letter like the good old days.

Mistake Number 3: Not giving an offer!

This one kills me to my core. This is the settlement letter that reads “hey consumer we have a great offer for you but I am not going to tell you what it is. You need to call me and let’s discuss it and after that I will tell you what I have in store for you”. With this letter not only do I think you have a potential UDAAP problem unless you have trained each collector to treat everyone the same and give each consumer the same discount but the 2nd problem is that NO ONE IS GOING TO CALL YOU. See MISTAKE NUMBER 2. I guarantee if you look at your results the only consumers that called where those already highly motivated. I would go so far to say they where planning on calling you already. In today’s world our margins are so thin we need to make sure we spend every cent wisely. I love providing multiple options to the consumer in the same letter. I will provide the consumer not only a settlement offer but a payment arrangement offer in the same letter. If the consumer looks at the letter and says “I wish I had that kind of money to settle this” I want to make sure right behind it they see my payment arrangement offer and say “but I can afford that”. We all have clients that tell us how long a payment arrangement can be. This letter might not be for those clients. When you are determining the length of the payment arrangement please keep one thing in mind. This might be the most important thing other than the stamp on the envelope. Understanding how much they couldn’t afford when they defaulted, PERIOD. I am not sure what the point is in mailing a letter asking the consumer to pay more than the amount was that they couldn’t afford in the first place. I know this is common sense but take a look at your letters you might be surprised. If the consumer owes $5,000 dollars and the debt was a credit card I know at minimum they had a monthly payment of $100 that they couldn’t pay. So why in the world would I mail a letter asking them to pay $200. With this example I would send them a letter offering them $50 a month. I would rather have a paying account than an non-paying account every day of the week and twice on Sunday.

Mistake Number 4: Not tracking your results!

We all know the definition of insanity. Say it with me…..doing the same thing over and over again and expecting a different result. If your letter stunk last year, I can smell it from here this year. If you didn’t get results from your mailing last year something has to change. As we already discussed that could be how your letter reads, are you making it easy for the consumer, is your offer affordable? You must test each letter and track the results. We code each letter separately as I am sure you do. We also code the “client instructed letters” as well. So when tax time comes upon us and the requests come in we immediately take a look at the prior year. How did the letter do? Did we cover our expense? Or worse did we get sued?

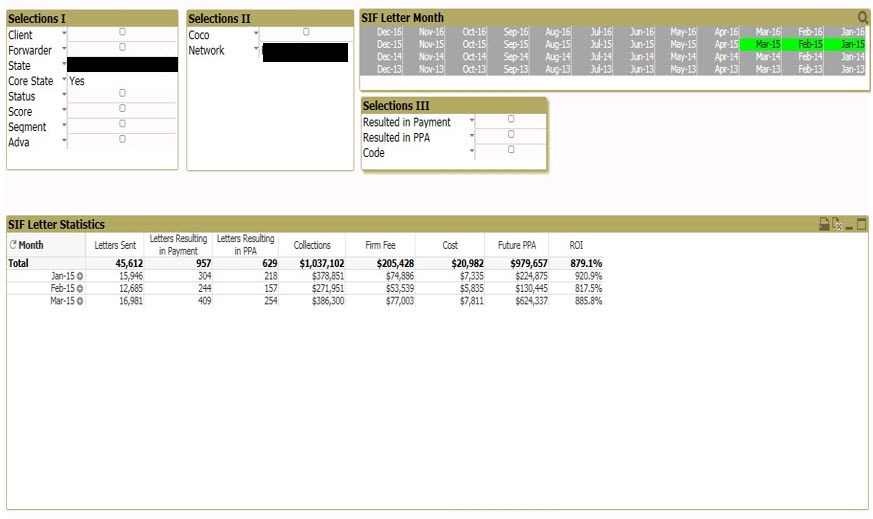

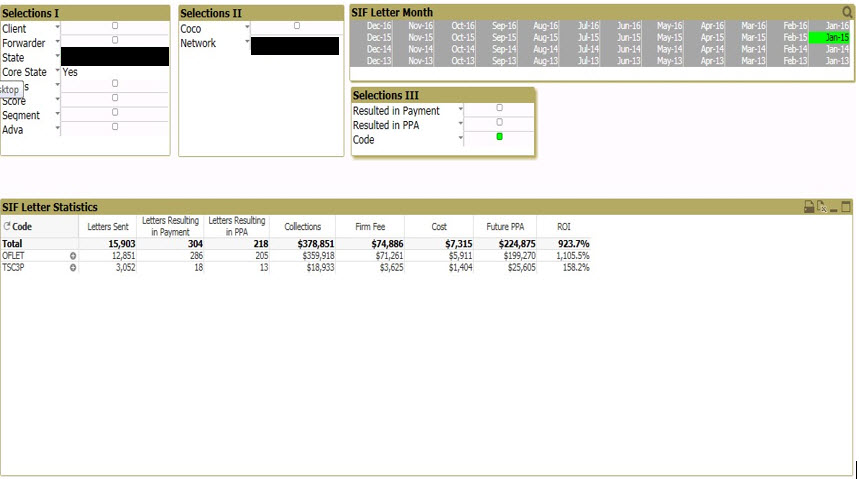

Here at Surefire we believe in operating smarter. There is nothing that brings a bigger smile to our face than when we can show a client how to maximize each stamp they put on. Below is one of our applications dedicated just to ROI. These screen shots show you by month and then by letter and exact results. If you would like to see more of what we can do give us a call.

Tracking Settlement Letter Campaign Statistics

Tracking Settlement Letter Campaign Statistics